Commentary

The Federal Reserve might have declared victory over inflation too soon.

We are barely a few weeks out from their new round of what was once called “quantitative easing” and prices on many items have already started to increase again.

The mechanism in play here involves a series of causally related steps. Congress spends money. Treasury marks it as debt, which the Fed purchases with new money and adds that to its balance sheet. The Fed lowers the interest rates it charges banks for loans, thus inspiring more lending, an easing that spreads to all debt maturities.

At the end of the process, and contingent on factors like the pace of spending and the pathways the new money enters economic life, the result with a lag is a lower value of the dollar in terms of goods and services.

The dollar is still strong internationally–its exchange rate with other currencies–which makes imports cheap and less susceptible to domestic inflationary pressures. Indeed, the imported goods inflation is far lower than the rate of dollar-produced goods. At the same time, the dollar has never been weaker domestically.

All of this sounds confusing and that traces to the changed meaning of words over time. A century ago, the definition of inflation was an increase of money and credit beyond the pace which output would normally require. Today we use the term inflation to refer to the effect: higher prices.

To be sure, there are some “exogenous shocks” that seem to be driving up prices–striking workers, migrant floods, government demand for services–but the Fed is supposed to be able to anticipate those when it formulates policy.

In this case, their easing stance runs the risk of setting off a second wave that could be worse than the first.

How bad was the first from 2021 to the present? We still cannot say for sure, partly because creating an index of trillions of possible inputs is impossible, and partly because the Bureau of Labor Statistics has been underestimating the pace of inflation for years, probably for political reasons.

The official data suggests that the dollar spent domestically has lost 20 percent of value from January 2021 to the present. That does not fit with industry data nor private experience. Industry data in groceries, rent, housing, cars, insurance of all kinds, and materials put the actual rates between 34 and 60 percent. A more accurate reading would need to include that which the Consumer Price Index excludes, including taxes, interest, and health and homeowners insurance.

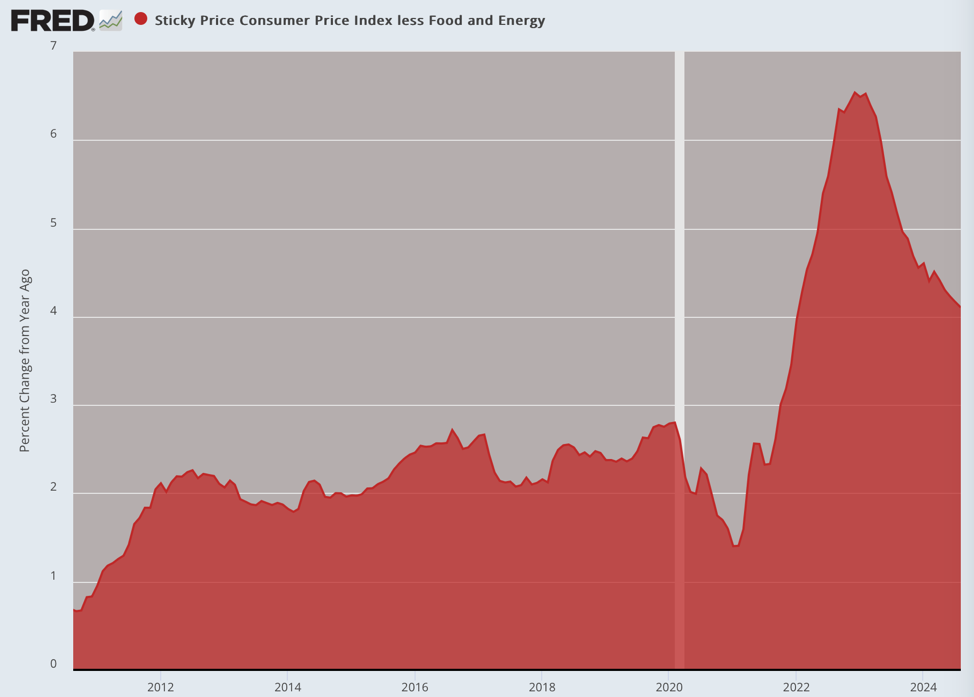

Even official data, however, once you exclude volatile sectors of food and energy, shows that the battle is not won. Inflation is running 4.2 percent at the most recent reading, which is more than twice the target. There is no sense in which inflation has been tamed to the extent any responsible monetary policy should desire.

How to discover where we are in real time?

For the better part of a year, the pace of price increases has slowed, which does not lower prices but at least makes them worse at a much slower pace. But in the last several weeks, we’ve seen a decisive shift in trends from below target to at target and then above target. Indeed the six month inflation rate according to this real-time tracker has again reached 3.1 percent, which is above 50 percent over target.

More importantly, this shift might represent a change in the inflationary dynamic from lower to higher.

The move is sudden and dramatic and is timed with the lower rates themselves, a policy which was designed to stop what the Fed believed to be an impending recession but carries the danger of kicking off a second wave of price increases that could be worse than the first one.

Already we see the physical results of the last wave. The grocery stores are filled with products in packages that are smaller than five years ago. This is called shrinkflation. If you doubt it, have a look at the size of a cheddar cheese ball this season compared with three seasons ago.

The BLS claims to track it but it is simply not possible to do so for the billions of product offerings out there. Another factor for dealing with inflation are higher fees, and they are everywhere these days.

Everywhere you spend these days, you encounter new processing fees, convenience fees, service fees, and strange impositions of charges for what used to be free. This deployment of fees to deal with price pressure and accounting squeezes is now embedded as part of our commercial lives.

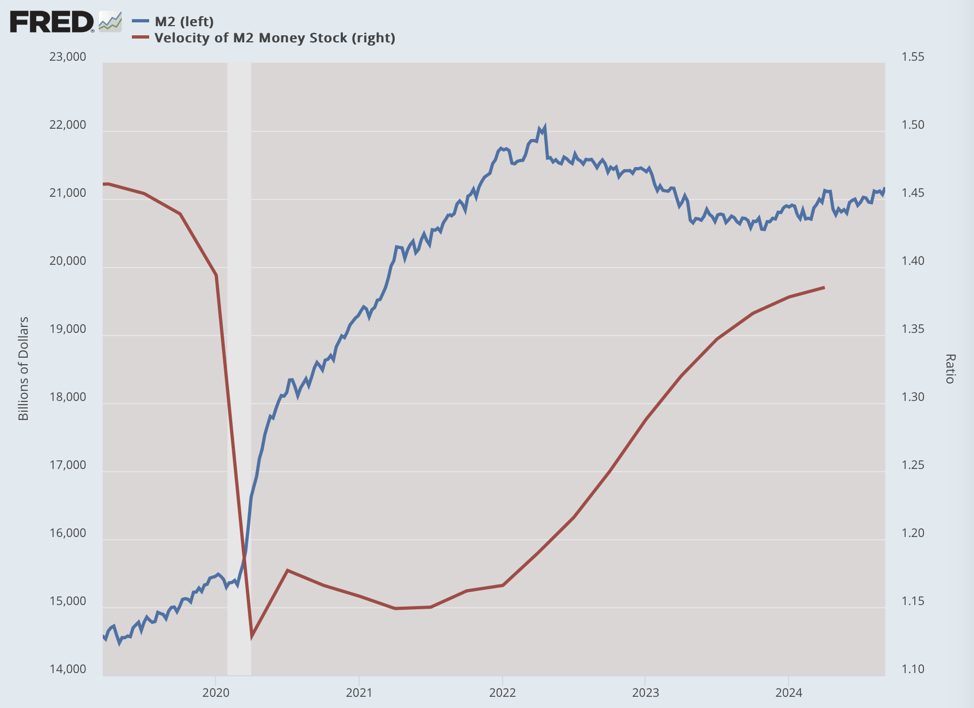

What is driving the re-acceleration of inflation now? There are a number of factors. The concept of velocity is a measure of the pace of spending–the economic equivalent of the transmission rate of viruses. Velocity always falls in a crisis as consumers and producers become risk averse. This puts downward pressure on prices. But as the economy comes out of crisis, velocity increases, which puts upward pressure on prices.

Velocity has been increasing for two years and continues to rise, even as the money stock is growing as well. This will certainly lead to higher inflation, precisely as we’ve begun to experience in the fall of 2024. Velocity has a long way to go to normalize, while the forced lower rates will certainly lead to ongoing increases in the money supply.

The great danger that presents itself is a repeat of the 1970s. The inflation of that decade came in three waves: 1971-1974, 1975-1977, 1978-1981. The first wave came with the end of the gold standard and the creation of the fiat dollar both domestically and internationally. The second wave came as a result of the suppression of price increases in the first wave. The third wave came once the Fed lowered rates on the belief it had conquered inflation already and would feed the economy to prevent recession.

One might assume that money managers would learn but it is a curse of the human project that one generation’s tragedies do not fully port over to the thinking and actions of the next generation. Half a century is apparently too long ago to offer a new generation any serious lessons.

Other factors are the profligacy of a Congress that cannot stop spending, an administration that demands an infinite supply of funds to sustain its military commitments, a public suffering and dependent on handouts, and a Fed which accommodates all of this through new money creation. What is also lacking are leaders who are willing to stand up and tell the truth: The United States must balance its budgets and the economy desperately needs a period of austerity to prepare for a new prosperity.

The real world impact is on the value of wages and salaries for American workers. The good life as we once knew it is no longer available for the majority of Americans. Home ownership is out of the question for anyone not among the top earners, while the debt load of the household keeps rising.

Savings rates right now are very low by any historical standard, while the costs of borrowing for consumers via credit cards is still centering on 22 percent. Carrying balances one month to the next is financially irrational but might be made necessary just to keep up with spending demands. And despite claims, there has been only a decline in real median household income over four years (the most recent increases depend entirely on false inflation numbers).

Current trends in monetary and economic policy suggest that the second wave will hit the United States hard next year, which will make the political environment highly volatile for any incoming administration.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.

Source link

Add comment