News Analysis

Money-supply growth rose year over year in November for the fourth month in a row, the first time this has happened since the four months ending in October of 2022. The current trend in money-supply growth suggests a significant and continued turnaround from more than a year of historically large contractions in the money supply that occurred throughout much of 2023 and 2024. As of November, the money supply appears to be entering a new and accelerating growth period.

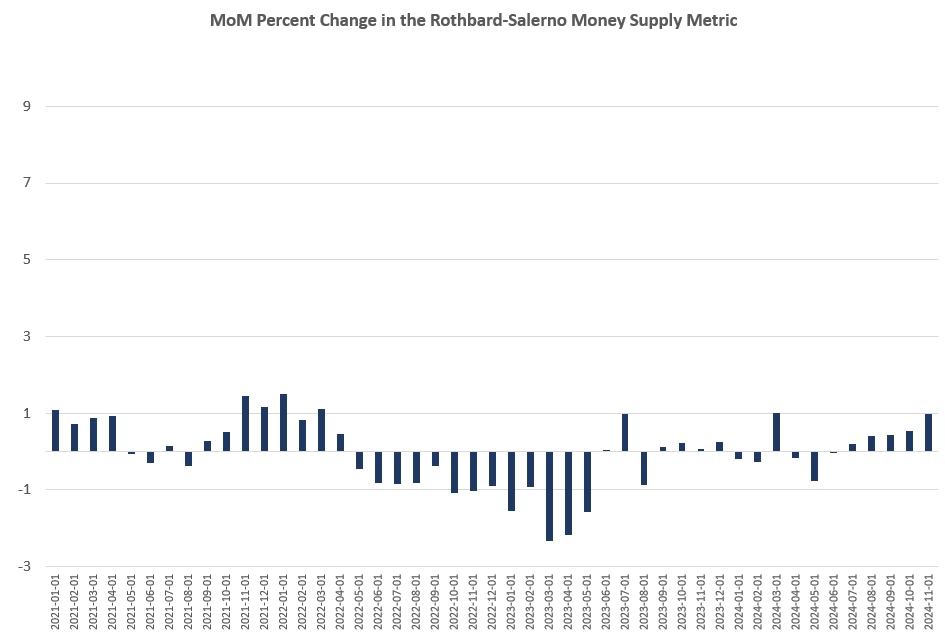

That downward trend now appears to be well over. Indeed, when we look at month-to-month changes in the money supply, we also find an upward trend. The money supply has increased each month from July through November of 2024. The money supply increased by 0.95 percent from October to November. That’s a nine-month high and is the third-largest increase since March of 2022.

Related Stories

In recent months, M2 growth rates have followed a similar course to TMS growth rates, although M2 is growing faster than TMS. In November, the M2 growth rate was 3.73 percent. That’s up from October’s growth rate of 3.13 percent. November’s growth rate was also up from November 2023’s rate of negative 3.27 percent. Month over month, M2 increased by 0.94 percent from October to November. That’s the largest month-to-month growth rate in nine months.

All that said, recessions tend not to become apparent until after the money supply has begun to accelerate again after a period of slowing. This was the case in the early 1990’s recession, the Dot-com Bust of 2001, and the Great Recession. This may be the trend we are seeing now.

Indeed, the acceleration in money-supply growth that we’ve seen in recent months corresponds with new efforts by the Federal Reserve to force down the target policy interest rate, thus spurring more money creation. In September, the Fed’s FOMC cut the target rate by 50 basis points. Such a sizable cut to the target rate is usually followed by a recession since the Fed usually only implements such a large cut when it fears an approaching recession. The Fed cut the target rate again in November, and then again in December.

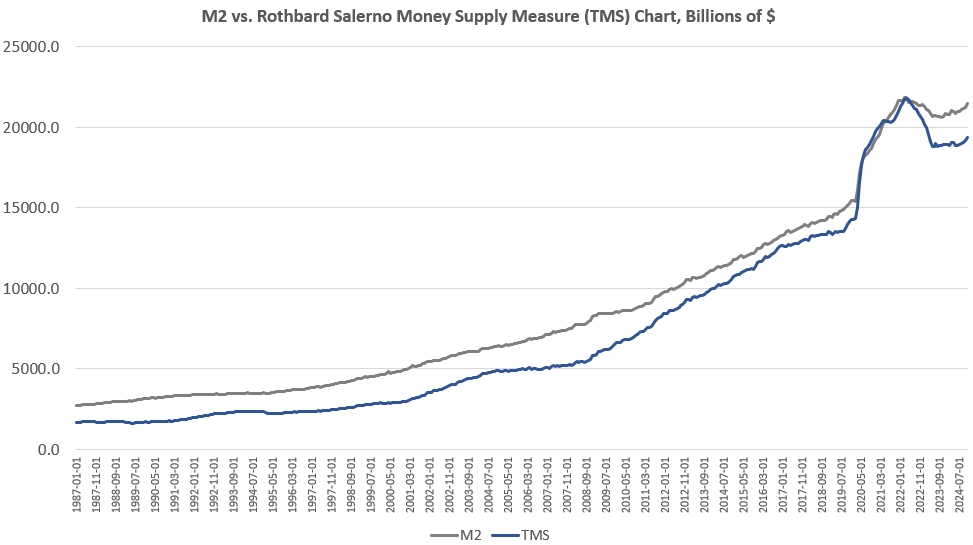

Moreover, the Fed’s return to dovish policy strongly suggests that the Fed has no plans to unwind the trillions of dollars it added to the economy over the past five years. In spite of last year’s sizable drops in total money supply, the trend in money-supply totals remains well above what existed during the twenty-year period from 1989 to 2009. To return to this trend, the money supply would have to drop another $3 trillion or so—or 15 percent—down to a total below $15 trillion. Moreover, as of November, total money supply was still up more than 35 percent (or about $5 trillion) since January 2020.

Since 2009, the TMS money supply is now up by more than 192 percent. (M2 has grown by 150 percent in that period.) Out of the current money supply of $19.3 trillion, nearly 26 percent of that has been created since January 2020. Since 2009, more than $12 trillion of the current money supply has been created. In other words, nearly two-thirds of the total existing money supply have been created just in the past thirteen years.

Apparently, the Fed now is quite comfortable with this, in spite of the fact that there is no sign of CPI inflation rates returning to the Fed’s arbitrary two-percent price-inflation goal. For example, both CPI and core CPI increased in November’s month-to-month change. The CPI’s year-over-year change increased to 2.7 percent in November. The core CPI remained flat at 3.3 percent over the same period. In other words, the Fed does not appear to be prioritizing reductions in price inflation rates.

Money supply changes and CPI rarely follow a linear or one-to-one relationship, but with the Fed returning to a policy of easy money, after adding trillions of dollars to the money supply in just a few years, we can expect this to fuel further increases to both asset price inflation and consumer price inflation in coming years.

The Fed and the Federal Government Need Lower Interest Rates

So, why did the Fed return to pushing down interest rates, even with so much covid-era money still sloshing around in the economy? One answer lies in the fact that the US Treasury requires low interest rates to manage its enormous $36 trillion debt.

The fact that the bond markets aren’t cooperating with the Fed suggests that bond investors expect what the central bank is unwilling to admit: that deficit spending is likely to keep heading upward, fueling price inflation as a result.

That is, many bond investors suspect that as deficits continue to mount, the Fed will be forced to intervene to mop up excess Treasurys in order to keep yields from rising to unacceptable levels. To make these purchases, the Fed will have to create new money, and bond investors know that is likely to lead to more inflation. Eventually, to combat this price inflation, the Fed will again be forced to allow interest rates to rise again. Thus, we now see rising longer-term rates.

The 20-year Treasury bond offered a grim warning as a selloff fueled by inflationary angst gripped global debt markets: 5 percent yields are already here.

“The US market is having an outsized effect as investors grapple with sticky inflation, robust growth and the hyper-uncertainty of incoming President Trump’s agenda,” said James Athey, a portfolio manager at Marlborough Investment Management.

Moreover, much of this “robust growth” is being fueled not by sound economic conditions, but by government spending. That translates into even more upward pressure in interest rates, and in future price inflation.

All of this reflects the new acceleration in the money supply, with the Fed’s apparent approval.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.

Source link

Add comment