Commentary

Four months ago, Brownstone Institute commissioned a study from two astute economists (E.J. Antoni and Peter St Onge) that sought answers to two pressing questions. First, what is a more realistic read on the rate of inflation over four years, one that includes all that the Bureau of Labor Statistics (BLS) excludes and corrects for rampant misreporting? Second, what happens when you adjust output (GDP) against that new number?

The goal of the report was to discover a more realistic look at where we are in the boom-bust cycle. This becomes especially important given the upheavals the nation has seen over four years. Some slippage in understanding is to be expected but it’s time we look back with clearer eyes.

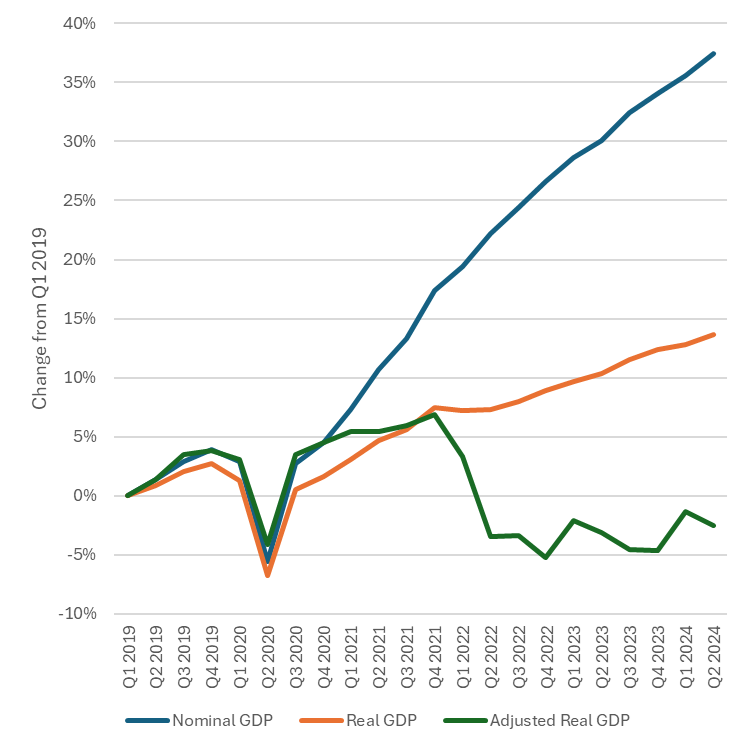

Once you adjust GDP to adapt it in real vs nominal terms, it reveals that we’ve been in recession since the first quarter of 2022. Indeed, 7 of the last 10 quarters have been net down in terms of economic growth. We’ve actually been witnessing a period of grueling recession, masked only by statistical illusion.

This judgment is not radical or a stretch at all. It reflects a growing consensus that the way agencies calculate inflation is plain wrong. It just so happens that it does not matter much either way in most times when prices are more-or-less stable and the target rate of 2 percent is the norm, as it has been for forty years.

The flaws in the system revealed themselves once inflation got out of control after the policy response of the COVID years, with its trend-busting spending and expansive monetary policy. Together with supply-chain breakages, the upward momentum in prices took hold and caused a reset of the purchasing power. Every sector in which there were problematic calculations was affected.

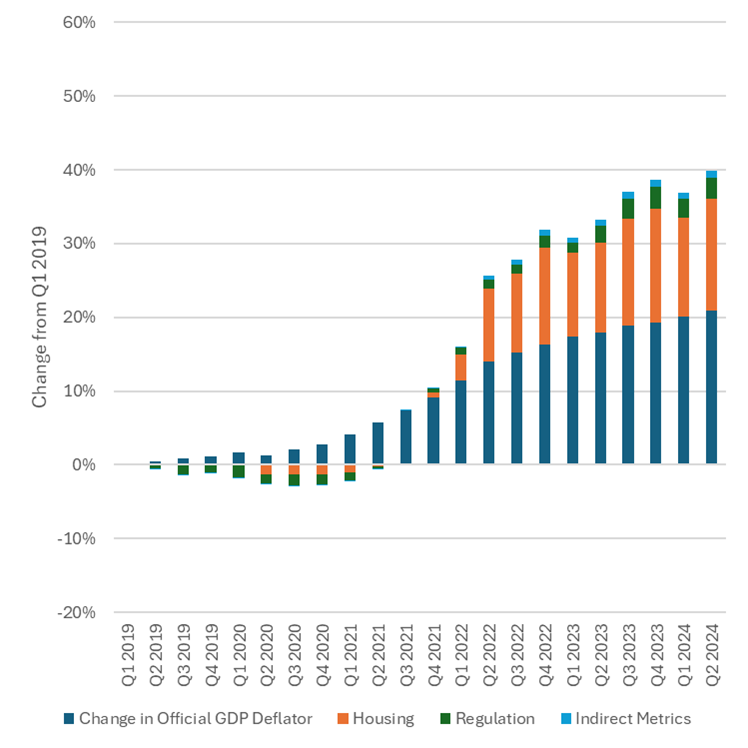

The report, for example, looks at the price of housing. The BLS does not report house prices, even though such indexes are readily available. Instead it looks at “owners’ equivalent rent,” which is a convoluted way of assessing value. The trouble with getting it wrong is that this sector is heavily weighted, fully 26 percent of the overall index.

As the report says, “If the costs to rent and own change commensurately over time, then this methodology will be relatively accurate. Unfortunately, the cost of owning a home has risen much faster than rents over the last four years and the Consumer Price Index (CPI) has grossly underestimated housing cost inflation. The cost of housing services in the National Economic Accounts published by the Bureau of Economic Analysis suffers from similar methodological problems.”

To be sure, you could say that actual housing prices don’t matter because most people are not buying. That’s true for jewelry at Tiffany’s too but their price changes are still relevant for building a price index. The point is to gather all information about final prices and build a measure of the loss of purchasing power for all goods and services. Grocery prices still matter, for example, even if many people have freezers full of meat and a garden out back.

Incredibly, the CPI does not consider housing insurance at all precisely because of this messy calculation. In normal times, perhaps one could say that this doesn’t matter. But in high inflationary times, the effect is to dramatically understate the realities.

Another problem relates to indirect purchases such as health care. The costs of insurance are measured against the goods and services consumed and finally assessed based on the profitability of providers. The report says: “Premiums are used both to pay for the actual cost of providing the service of insurance (risk mitigation) and for medical services and commodities. The CPI neglects both, and instead imputes the cost of health insurance from the profits of health insurers. If those profits decline because of increased costs of doing business for insurers, then this will register as a reduction in health insurance costs to consumers, even if premiums and coverage remain precisely the same.”

This is why health insurance premiums were reported as going down even at a time when they were obviously going up.

There are additional problems related to “hedonic” adjustments that regard all regulatory compliance as a net positive for quality. The report removes those by examining regulatory costs directly.

Making all these changes creates a different picture of inflation than we are getting from official data, stretching to a 40 percent loss.

What Antoni and St Onge have done is work from this precedent and they made additional corrections.

This adjustment affects the real value of income and output over the same period. The conventional wisdom is that we have been in a growth stage for years, with people like Paul Krugman claiming that the economy is in fine shape and that Bidenomics has worked out wonderfully.

Antoni and St Onge say that this is just an illusion. The supposed growth has been merely inflation. If you use the revised inflation data as the GDP deflator you generate very different results. Instead of a long period of growth, you end up with a long period of decline.

They document modest growth in 2021 as the nation recovered from lockdowns but that dramatically reversed in the first quarter of 2022 as rising inflation ate up the value of the seeming growth. The result is a full-on recession that has not receded.

In business cycle theory, recessions are marked by two successive quarters of decline in real GDP. That indeed did happen in 2022 but the recession was not declared based on the strength of the labor market. This study reveals that the recession was not only real but continued for the next two and a half years. We have to wait for third quarter data to come in before making any definitive declarations about the third quarter of this year.

Over this same period, American culture has grown weary of certified experts deploying data in defense of their plots and plans. Whether on COVID or on climate change, many of their claims and much of their data and models have been debunked. It’s long past time to apply this same incredulity to matters of economics. That is precisely what this study has done.

In private, most financial and economic analysts will admit that the inflation and growth data for years is not credible. But as a matter of conventional wisdom that you hear on mainstream media, the official numbers continue to dominate public culture. This is the only reason why it is widely assumed that we are in a period of economic recovery. Nothing on the ground suggests this. Not even the labor markets look healthy once you examine the details.

From my own perspective, these numbers are not only plausible; they likely understate the problem. This study does not correct for inconsistencies in government data over industry data in restaurants, cars, and groceries. It does not correct for shrinkflation oversights and new fees.

Additionally, this study does not attempt to remove government spending from the GDP numbers. Doing so would dramatically reduce the baseline output numbers, and produce a much deeper recession. For example, in 2023, government spending accounted for fully 34 percent of the GDP calculation.

Taking this extra step would likely change the depths from recession to outright depression. That might be a closer approximation of where we are. Still, this study is a first look and entirely consistent with evidence as we know it.

This is the first study to take a closer look at the strength of the U.S. economy over four years with an eye to precision and accuracy. The results are both shocking and not: yes, they contradict official messaging but they do not contradict public sentiment. After all, consumer sentiment is far lower today than before lockdowns. It continues to fall.

The National Bureau of Economic Research is charged with charting business cycle trends in the United States. It’s long past time for their models to acknowledge that many actual experts have begun to raise serious questions about the way government agencies are gathering and reporting data. If the results of a certain way of doing things simply stop explaining the world around us, it is time to reassess, regroup, and tell a truth that more closely fits the evidence.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.

Source link

Add comment